Second, go into the Area code on the possessions. When your Area code boasts more than one state, the house loan calculator commonly allow you to be choose the correct one to. To confirm the fresh county, take a look at assets record. The borrowed funds calculator requires the Zip code additionally the state during the acquisition to determine suitable property income tax rates.

5. Credit rating

If you don’t know your current credit score, score a copy of the credit history. Then click the dropdown menu and choose the range that includes your credit score.

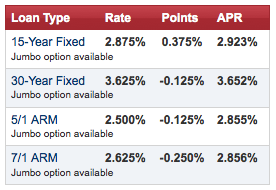

Your credit rating is certainly one factor regularly figure out which mortgage facts you could potentially qualify for. Really loan providers give you choices based on your credit rating and you will other variables such as your month-to-month earnings plus debts. When you yourself have a credit history out of 740 otherwise over, it’s also possible to be pop over to this site eligible for a lesser interest rate.

6. Financial needs

So you can understand the right financial alternatives for their means, buy the component that matters really for you. Examine these alternatives:

- Low interest: Gives the reduced you can easily interest rate, regardless of the lifetime of your financing.

- Steady payment per month: Holds a similar interest rate towards the duration of the mortgage having a predictable monthly payment.

- Short-identity ownership: Allows you to protect a lowered interest toward first couple of several years of your own home loan before transitioning so you’re able to an adjustable rates.

- Reduced payment per month: Gives the littlest you’ll be able to payment, which need a longer mortgage title.

seven. Assets type of

For more okay-updated mortgage choices, click the Advanced relationship to address several even more concerns. After that discover the brand of possessions you plan to finance. Choices is:

- Single-house

- Condo

- Co-op

- Two-family home

- Three-home

- Four-family home

Mortgage loans without a doubt assets versions generally have different interest rate ranges. For example, single-family homes often have lower interest rates than condos. Not all lenders offer mortgages for condominiums, so there’s less competition, and mortgages for condominiums are somewhat riskier than for single-family homes.

Next, choose whether you plan to use the home as your primary residence, a next or trips home or a rental or investment property. Lenders may offer different interest rates based on your intended use. For example, interest rates for investment properties and vacation homes are often higher than those for primary residences.

nine. Personal data

Click the circles to indicate whether you’re a United States citizen or a first-time homebuyer. If both, you could qualify for certain home loan products. For example, you might be eligible for a loan from the Federal Housing Administration (FHA). Since they typically offer low down payment options and low closing costs, FHA loans are often more affordable.

10. Possessions fees

Though annual assets fees you should never alter simply how much you acquire, they do impact your own homeloan payment. Extremely lenders are one-twelfth of your own yearly possessions tax from inside the for every single month-to-month homeloan payment. Then they afford the income tax on the county for you.

eleven. Homeowners insurance

Next, go into the homeowners insurance advanced you will have to shell out per month. To track down which count, you could label your insurer. Your own insurance carrier may bring a great calculator on their website.

Instance property tax, home insurance will not connect with the loan number. Yet not, really lenders tend to be it on your homeloan payment, upcoming afford the premium for you.

several. HOA costs

Ultimately, enter the month-to-month HOA charges. You will find this post towards the possessions listing, that ought to mean should your house falls under a keen HOA and you will people applicable charge. If your house has no an enthusiastic HOA, get-off this area empty.

Scrivi un commento